Facts and Figures

What is the share of ITHs in world trade?

According to statistics commerce accounts for about 20 % of the total figure of exports/imports + commercial services worldwide. For the sake of accurate information this is the break down of the annual figure at the end of 2019.

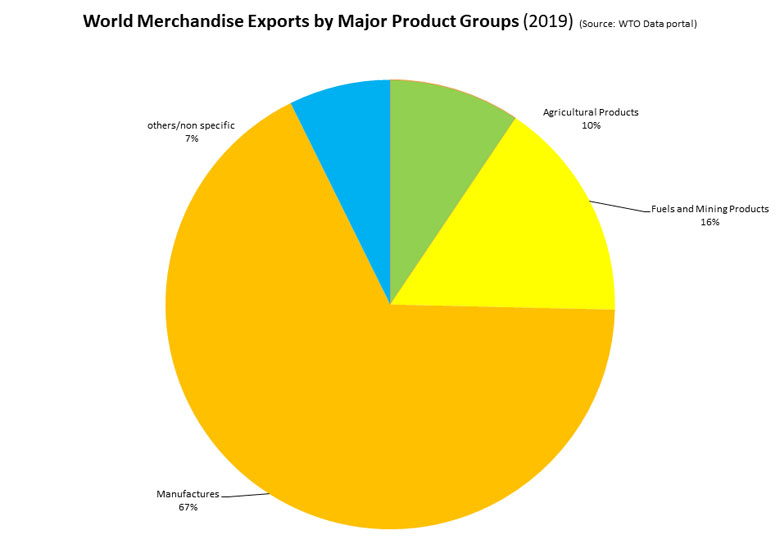

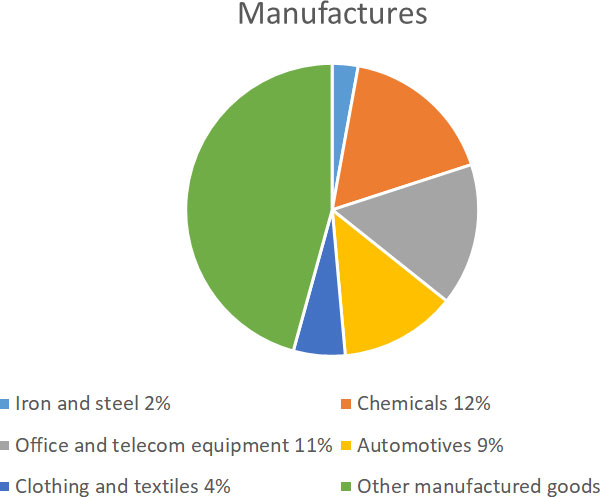

Merchandise Trade

Following declines in 2015 and 2016, the value of world merchandise exports increased in 2017 by 11 per cent. This trend continued until the beginning of 2020, when the worldwide Covid-19 pandemic led to a decrease in Q1 2020 by 11 percent in comparison to Q4 2019 and a further decrease of another 13 percent in Q2 2020. The numbers have increased by 21 percent again by Q3 2020. With the second wave of COVID-19 in the winter of 2020, these numbers will most likely decrease again.

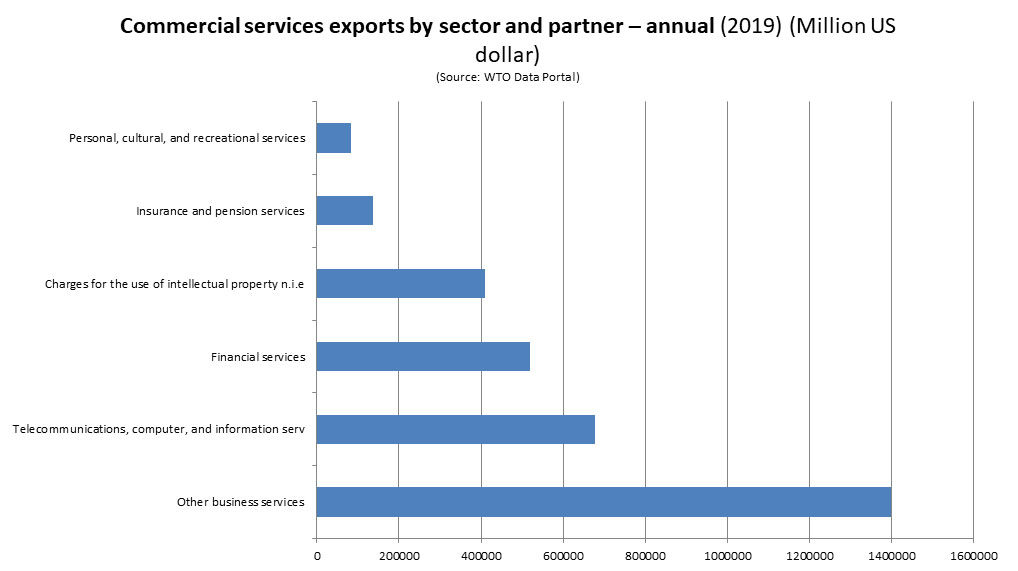

Trade in commercial services

World exports of transport services made full recovery in2017, supported by an increase in merchandise trade flows. World exports reached US$ 931.5 billion by going up 9 per cent. In Europe, which accounted for almost half of global transport exports in 2017, transport revenues went up to 11 per cent.

Trade in the EU

The EU is the largest economy in the world. Although growth is projected to be slow, the EU remains the largest economy in the world with a GDP per head of 25.000 Euro for its 500 million consumers. Furthermore it is the world's largest trading block and the world’s largest trader of manufactured goods and services.

The EU benefits from being one of the most open economies in the world and remains committed to free trade. The average applied tariff for goods imported into the EU is very low. More than 70% of imports enter the EU at zero or reduced tariffs. The EU’s services markets are highly open and we have arguably the most open investment regime in the world.

In almost all EU Member States, the main partner for exports of goods in 2019 was another member of the European Union, except for Germany, Ireland, and the United Kingdom (the United States was the main destination of exports).

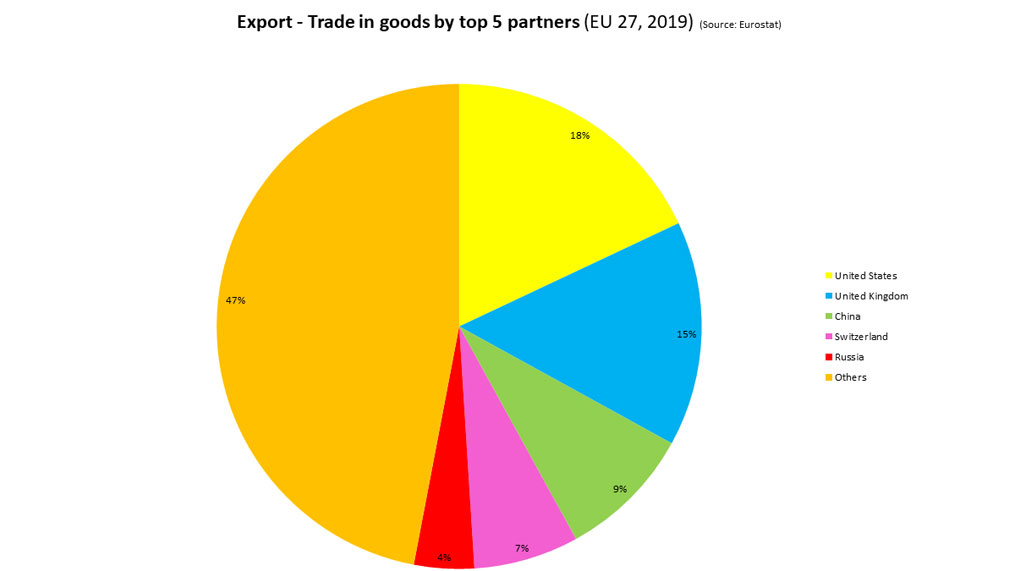

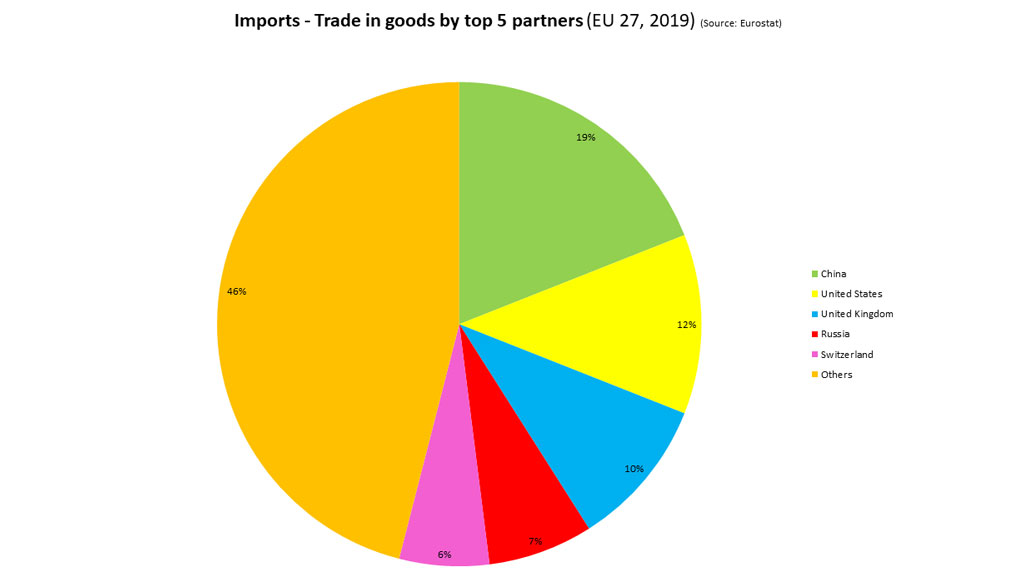

Overall, Germany was the main destination of goods exports for 17 Member States. For extra-EU trade, that is trade with non-EU countries, the main destinations of EU exports in 2019 were the United States (18% of all extra-EU exports), China (9%) and Switzerland (7%). With Brexit, the United Kingdom now hold the status of a third country and is therefore becoming the second largest extra-EU trading partner (15%).

In the first eleven months of 2020, China was the main partner for the EU. This result was due to an increase of imports (+4.3%) and exports (+1.1%). At the same time trade with the United States recorded a significant drop in both imports (-13.0%) and exports (-9.3%)

The EU's main import partner is China. Its share increased from 15 % of total extra-EU imports in 2009 to 19 % in 2019. Imports from the United States make up 12 % of the imports.

Impact of COVID-19

International trade has been directly affected by the impact of the COVID-19 pandemic. Travel restrictions and border closures have disrupted freight transport, supply of services and business travel. Travel restrictions are therefore likely to account for a substantial increase in trade costs for as long as they remain in place. Additionally, the closure of national borders and the disruption of the free flow of goods and services within the European Union have shown the fragility of the single market.

Freight transport service performance is crucial to trade costs in manufacturing. Since the beginning of the COVID-19 crisis, maritime and land transport have remained largely functional according to the World Trade Organization.

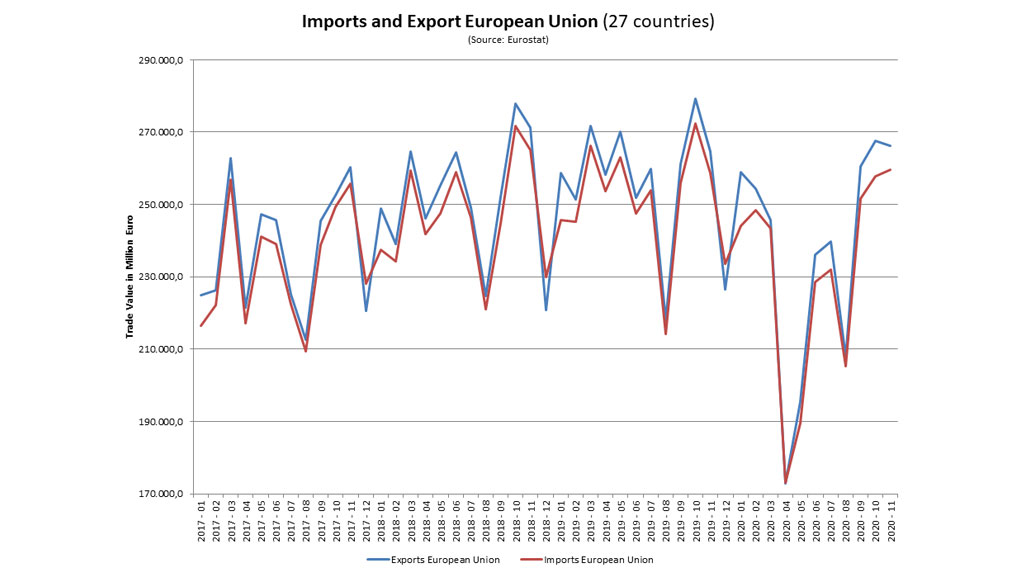

In January to November 2020, extra-EU exports of goods stood at 1.756,6 billion Euro (a decrease of 10.3% compared with January-November 2019) and imports at 1.569,4 billion Euro (a decrease of 12.3% compared with January-November 2019). As a result, the EU recorded a surplus of 187,2 billion Euro, compared with a plus of 169,4 billion Euro in January-November 2019. Intra-EU trade fell to 2.605,3 billion Euros in January-November 2020, minus 8.4% compared with January-November 2019.

Confederation of International Trading Houses Associations (CITHA)

Headquarters

Avenue des Nerviens 85, 3rd floor, B-1040

Brussels/Belgium

Please contact CITHA in Germany via

Confederation of International Trading

Houses Associations (CITHA)

c/o BDEx

Am Weidendamm 1A

10117 Berlin, Germany

Phone: +49 30 72 62 57 93

Fax: +49 30 72 62 57 94

E-Mail: info@citha.eu

© 2019 Confederation of International Trading Houses Associations (CITHA)